2025/09/13 エディンバラ外交経済学院 Briefing

Edinburgh Institute of Diplomacy and Economics Briefing

ー一時的な利下げ期待と相対的安全性からアメリカAIセクターへの資金流入。安全保障環境と政策不透明性からの安全資産上昇。

安全資産に投資妙理。景気後退はあっても金融危機は回避できるだろう。

capital inflows into U.S. AI stock market from expected temporary rate cut and relative safety. Capital inflows to safe assets from global security environment and policy uncertainty. Safe asset investment attractive.

Stagflation is plausible, but financial crises can be averted.

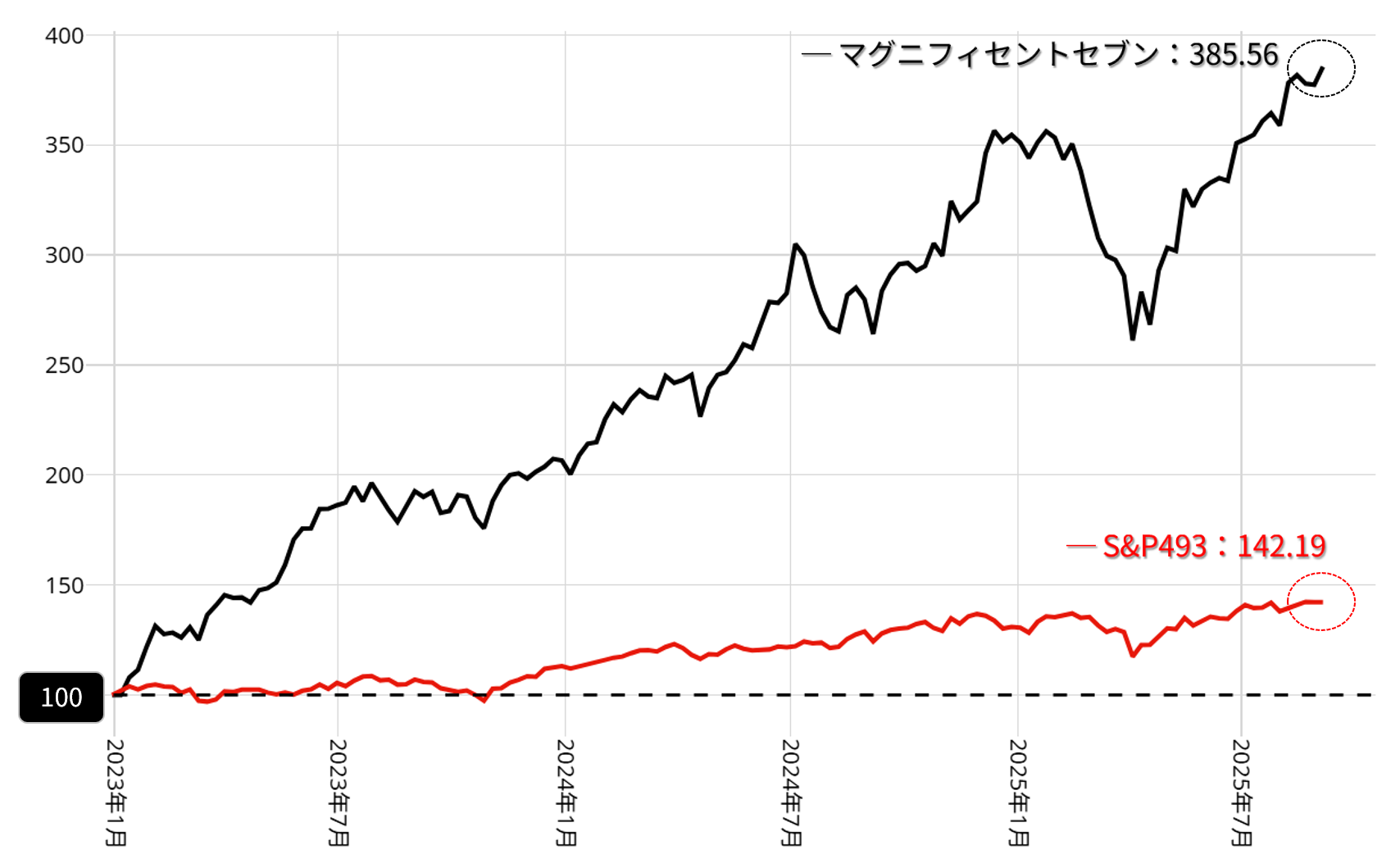

<ハイテクセクター主導の株価上昇ーhigh-tech equity driven stock prices>

マグニフィセントセブンとS&P493のプライスリターン:日次 2023年1月~2025年9月9日

IG:米国株見通し(9/10):S&P500最高値更新、6600視野も 米PPI・CPIに注目

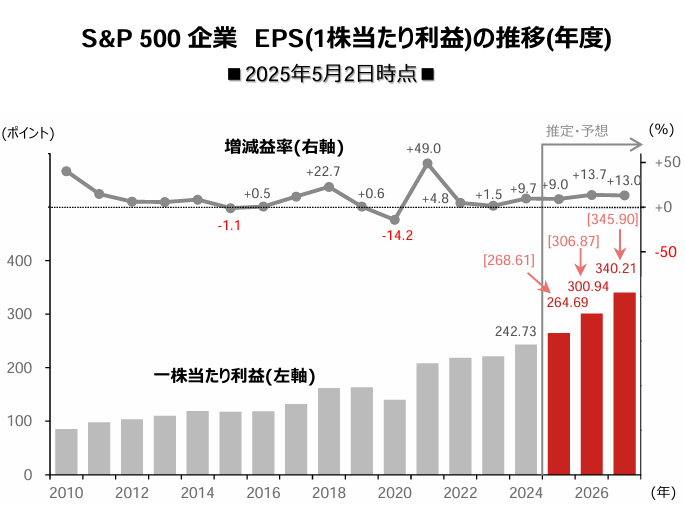

<2025年5月2日時点(As of May 2th)のS&P500指数構成企業のEPSの推移>

(注)予想はLSEG集計による2025年5月2日時点の市場予想平均。

(出所)LSEGより野村證券投資情報部作成

<日米株高の背景-Stock rally of U.S. and Japan>

9/4のレポートで書いたようにアメリカ景気はスタグフレーションに突入しそうだが、「奇妙な均衡」が保たれておりFedは年内に一度は利下げをするだろう。

AIセクターが牽引するアメリカ株の影響を受けて半導体セクターの寄与度が高い日経平均も上昇を続ける。

資産効果で好循環が続いていることも株価上昇の背景にあるのであろう。

As written in the report on September 4th, Fed is expected to cut interest rate once this year in the midst of queer equilibrium in spite of the economy falling into stagflation.

Thus AI-led U.S. stocks rally continues with the rise of Nikkei mainly composed of semiconductor sector equities.

The wealth effect is considered to be another factor circulating the stock market moving upward.

9/11の東京マーケットでは日経平均が600円ほど上昇したが、値がさ株のSBGとアドバンテストが500円程度を押し上げる歪な構成だ。

またフランスの政情不安やロシアからの安全保障リスクにさらされているヨーロッパから日本株にも資金が流入している。

フランスは深刻な財政リスクを抱え長期金利は急上昇しており今後の格下げの可能性も排除できない。

Nikkei rose around 600 JPY on September 11th, but what should be noticed is only two high-tech stocks, SBG(9984) and Advantest Corporation(6857), contributed to the rise of about 500 JPY.

Furthermore, money flows from Europe responding to security risk from Russia and political uncertainty in France.

Fiscal deficit is surging and long-term French gov yield reaching the concerning-level.

Downgrade of gov debt cannot be plausible.

不動産がGDPの6割を占める中国でも行場のないマネーが香港市場やアメリカの不動産市場に流入している。

最後にインドであるがアメリカからの高関税を課されても内需主導の経済であり、対米輸出は全輸出の2%程度に過ぎずGDPの下押し圧力としてはマイナス0.2%ー0.4%と見積もられている。

問題はあるが生産年齢人口は伸び続ける民主主義国で英語が共通言語であることから、チャイナリスクを避けるために資金が流入しているのだろう。

Real estate constitutes 60% of Chinese GDP, but the slowdown in this sector is a driving force to push money to financial markets of Hong Kong and U.S. real estate.

Finally, speaking of India, tariff-imposed India is a domestic-driven economy and the negative effect of high U.S. tariffs is estimated from 0.2%-0.4% of GDP considering the mere 2% of export to the U.S of the total.

Despite many socioeconomic obstacles, India attracts money because of the increasing working population, democracy, English-speaking country and China-risk.

<安全保障環境と安全資産-security environment and money flows to safe assets>

<Prices of silver and platinum as of 13th June 2025>

source-Financial times

‘’Platinum Leaves Gold Behind. Forecast as of 13.06.2025’’>

まず中東においてはアメリカが支援する西側の同盟国であるイスラエルがガザでジェノサイドを続ける。

しかし同盟国に対する国際的な制裁は前例も乏しく難しい。

(記憶に新しいのは南アフリカのアパルトヘイト政策に対する経済制裁であるが、制裁網構築にも問題解決にも数十年かかっている。)

主導権を発揮することが最も期待されるフランスも政情不安で外交政策に抑制がかかる。

In the first place, US-sponsored Israel keeps committing genocide in Gaza.

However, exerting international pressure on allies is rare in history and encompasses obstacles.

The most prominent France to take the initiatives is constrained by domestic political turmoil.

またロシア・ウクライナ戦争でNATO内でアメリカとEUの対応策での根本的な差異が見られる。

規範重視のヨーロッパと商業主義のアメリカ政権の分断ということである。

Also, the difference in foreign policy posture inside NATO is apparent in the Russian-Ukraine war.

European countries lay emphasis on norms, on the other hand, the Trump administration takes commercial-oriented politicoeconomical policy.

この分断がプーチンにとって最善の機会であり、最大限に利用していることで両紛争は停戦の兆しが見えない。

Vladimir Putin takes full advantage of this division, leading to the continuation of wars.

このような安全保障環境の元、安全資産へも資金が流入している。

まず金が急騰し、史上最高値の1オンス3600ドルをつけた。

そして出遅れていたプラチナやシルバーの価格も上昇している。

安全通貨であるスイスフランも増価した。

しかし輸出が不利になりスイス経済には打撃となっている。

不透明な安全保障環境とアメリカの政策不透明性から、各国の中央銀行の購入による金の価格はまだ上昇の余地があるであろう。

The security environment above mentioned drives money into safe assets.

First, gold prices started to surge to record-high $3600, followed by price hikes of silver and platinum.

Also, the Swiss franc appreciated, which had a detrimental effect on the export-led Swiss economy.

The risky security environment and uncertainty of U.S. economic policy are expected to continue driving up the prices of gold through the purchase of gold as a part of their portfolio reallocation from dollar assets of central banks.

現在のサプライチェーンは最適な構成ではない。

The current global supply chain is not the most appropriate structure.

世界経済が巡航速度で回復基調に載るためには、出口が見えない両紛争の解決が不可欠である。

Termination of two ongoing wars is essential for the world economy to grow faster and steadily.