2025/09/04, Edinburgh School of Diplomacy and Economics, Briefing

- The “peculiar equilibrium” of dictator Trump's policies (tariff policy, immigration exclusion policy) will collapse.

The Federal Reserve will likely cut rates once, but thereafter maintain high interest rates under stagflation.

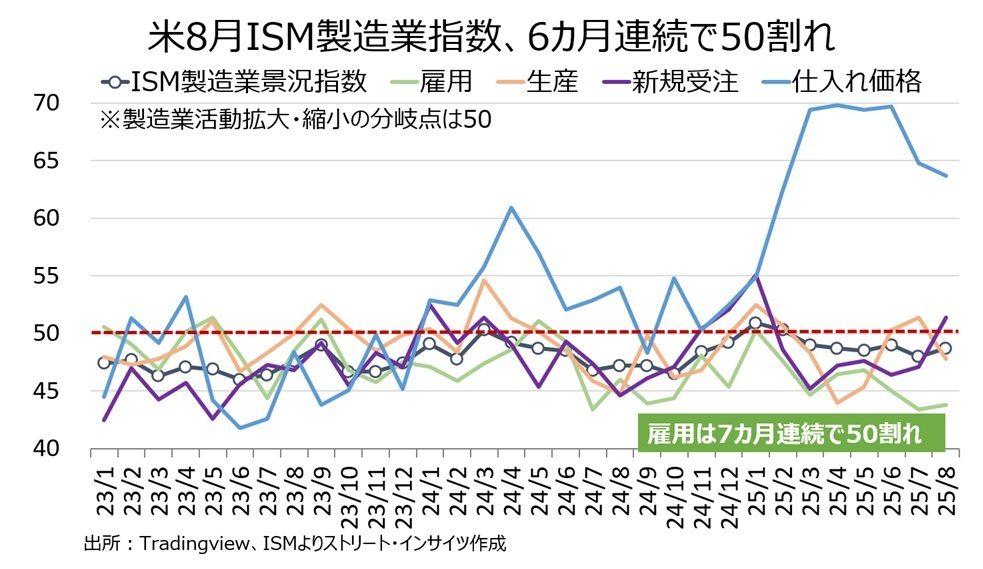

The July 2025 ISM index has been trending below the previous benchmark of 50.

Capital expenditure remains robust for AI-related intellectual property investment, but construction investment declines due to lower energy market conditions.

Two points warrant a particular note.

First, notably for both manufacturing and non-manufacturing sectors, the leading price index for purchasing remains at elevated levels comparable to those seen during the COVID-induced inflation of autumn 2022.

The employment index also shows subdued trends.

<Purchase price=仕入れ価格, Employment=雇用>

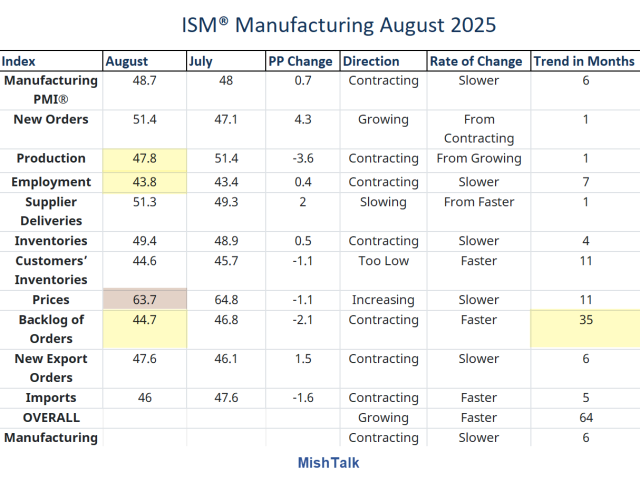

<ISM Manufacturing August 2025>

The likely background factors are Trump's tariff policy and immigration policy.

US companies bear 87% of the tariff impact, with earnings deterioration observed in August; full-scale price pass-through is expected to commence going forward.

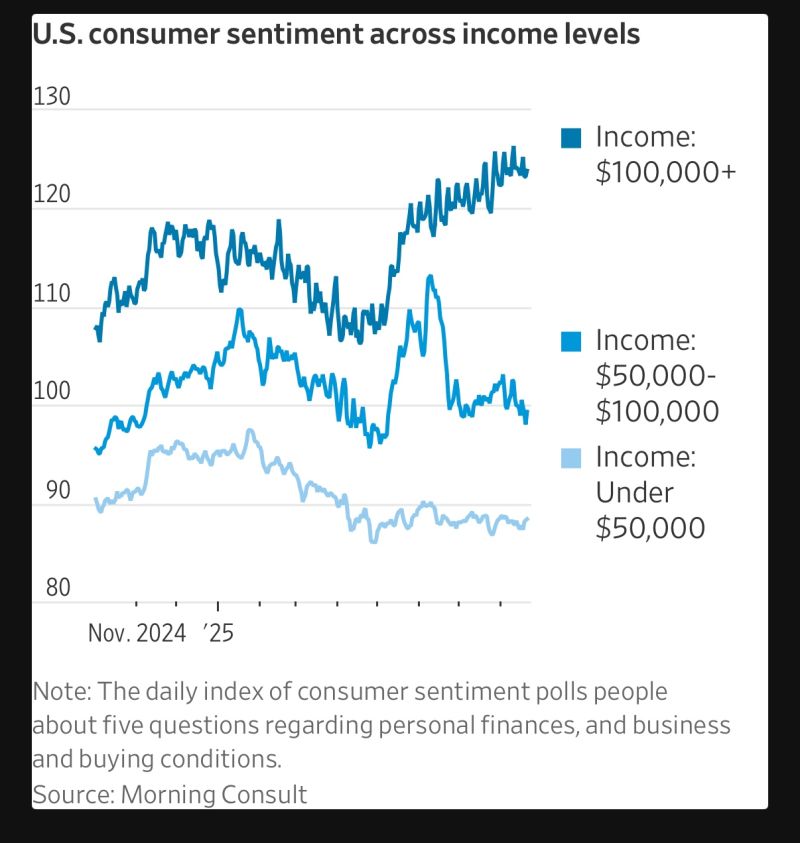

The deterioration in consumer sentiment among those with incomes below $100,000 is pronounced.

<US consumer sentiment by income level>

Household inflation expectations are also rising.

However, inflationary pressures remain less visible because price pass-through is occurring primarily in businesses targeting affluent consumers, where current consumption exhibits low price elasticity.

(Price pass-through is 1.6 times more advanced in businesses targeting affluent consumers than in those targeting the general public.)

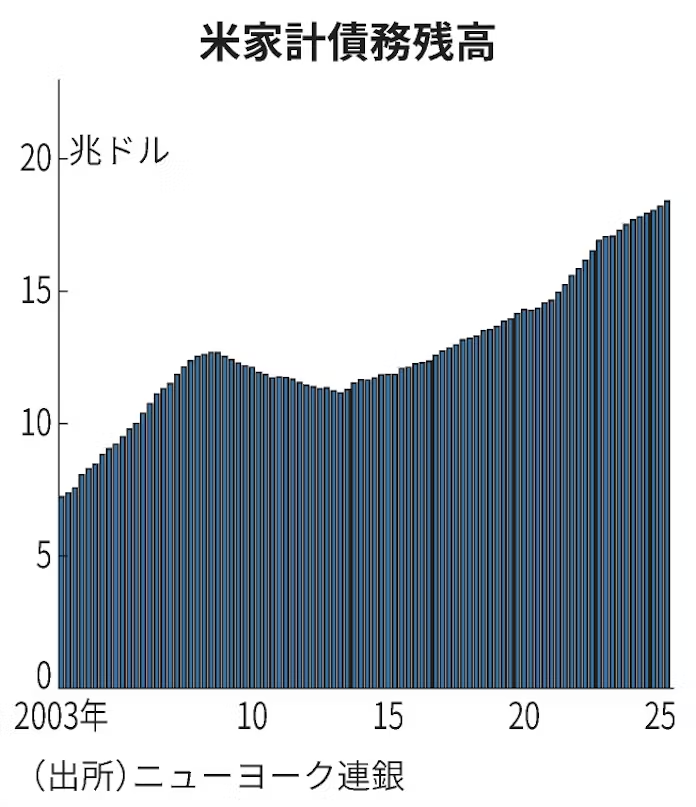

Swollen household debt (delinquency rates on student loans and credit cards) is also a concern.

<Household debt>

Vertical axix:Trillion USD、Horizontal axis:period from 2003-2025

<Federal Reserve Bank of New York>

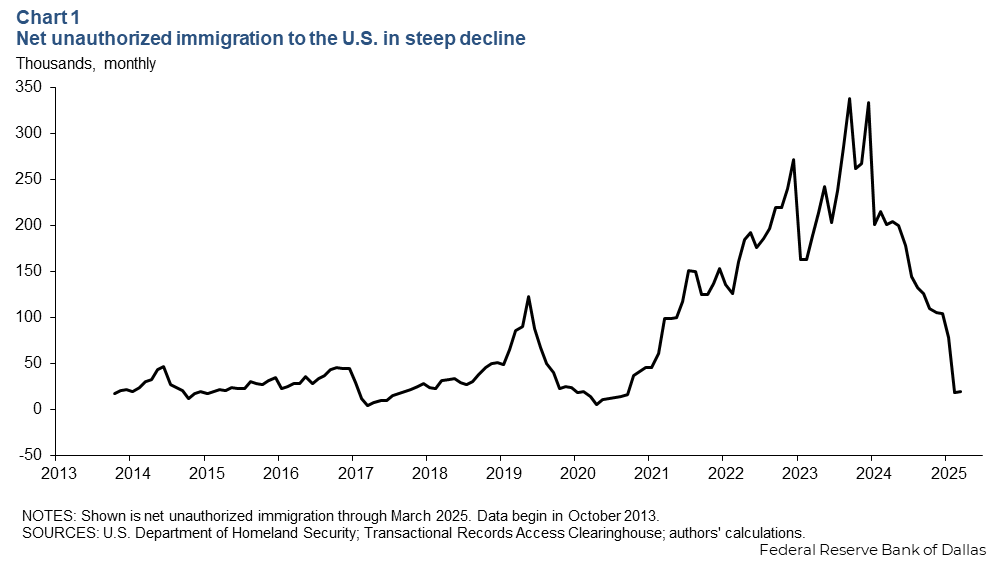

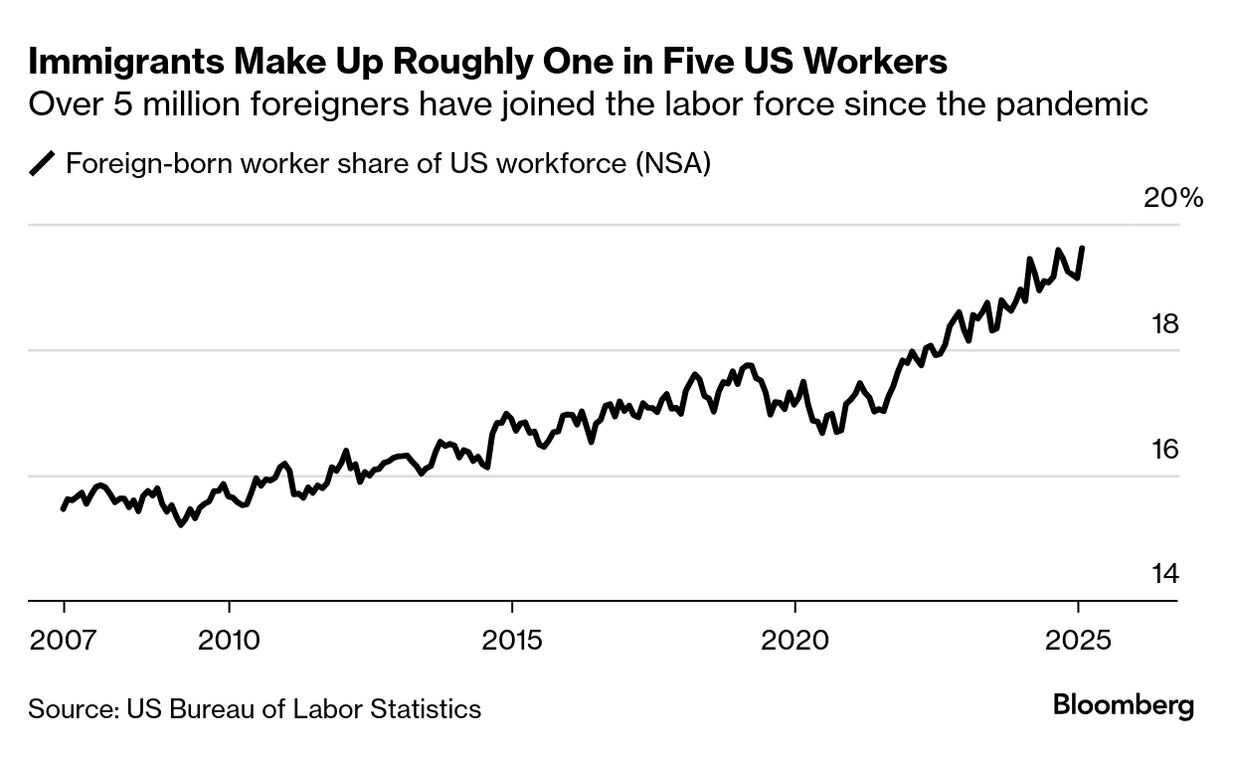

Next, let us examine the impact of immigration policy.

The number of foreign workers, who tend to have higher labour force participation rates, has decreased by one million from its peak.

This has two aspects.

First, 70% of immigrant workers live in rental accommodation, double the US average of 35%.

The rental market is experiencing a moderation in supply and demand.

Another crucial aspect is the impact on employment.

Immigrants constitute 20% of the American labour force.

Moreover, the construction and agricultural sectors are industries that cannot function without immigrants, and a sharp decline is evident.

Additionally, recent restructuring in the high-tech sector, driven by labour-saving measures using AI, is progressing.

Policy uncertainty reduces labour demand, while declining immigration reduces labour supply.

Furthermore, the non-working population aged 16-34 is shrinking as young people exit the labour market due to employment difficulties.

This decline in labour participation is the backdrop to the persistently low unemployment rate.

The economy happens to be at a point where rate cuts are appropriate now, but going forward, tariff and immigration policies will likely cause an economic slowdown first, followed by renewed inflationary pressures.

The Federal Reserve will probably cut rates once, but thereafter, it may raise rates again under conditions of stagflation.

<Declining unauthorized immigrants>