July 13, 2026

EIDE Briefings

ーThe future of Iran War and portfolio management till Nov

WTI and equity markets

Buy more share when the share price falls

Despite the ceasefire between the United States and Iran, both sides continue the limited war while considering their domestic situations.

Many may worry about the fragility of the agreement, but too much pessimism over the financial markets is unnecessary.

Both parties realize they have to coexist in the end.

For the first time in a decade, senior officials of both parties met.

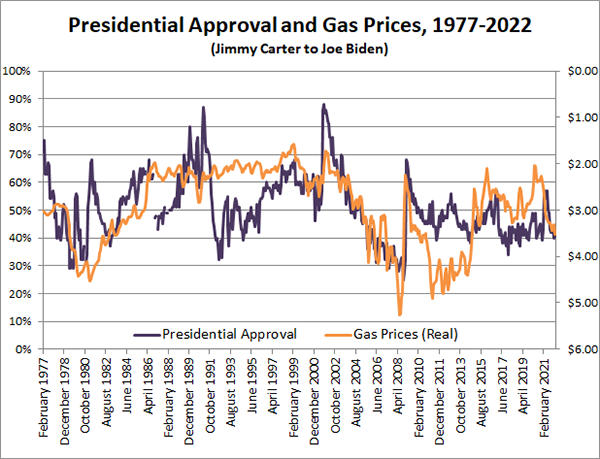

For Trump, he has to contain the inflation rate within a certain range considering the coming Midterm election in November.

<Negative Correlation between gas prices and presidential approval>

Gas Prices and Presodential Approval by Kyle Kondik

https://centerforpolitics.org/crystalball/gas-prices-and-presidential-approval/

That is why he is acquiescent to hawkish FRB chair Warsh in spite of his insane and furious military operations against Iran.

For Teheran, they have to prevent the outbreak of the public uprising as a result of economic hardship.

At least till the Midterm election in November, sporadic limited conflict and negotiation are expected to continue.

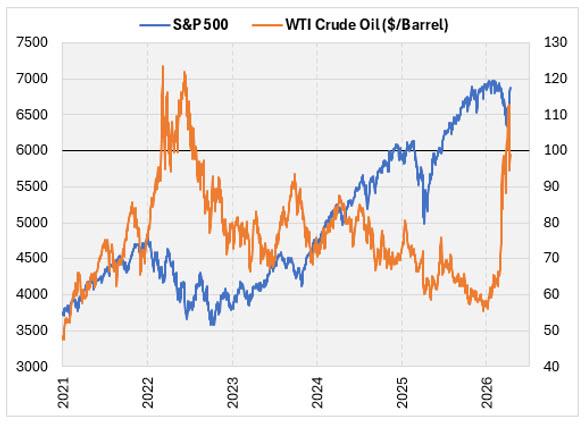

Negative correlation can be found between S&P 500 and WTI.

Thus manipulated military operations will keep the WTI prices between $60-$80.

(Turbulence of the equity market comes as a result of the oil prices over $80, which signals a crisis)

In general, a mild upward trend is going to continue with risk-on and risk-off posture mixed.

<Negative correlation between WTI prices and share prices>

Expensive Oil Not a SPX Death Sentence, But Bad Enough

High oil prices have historically been a major headwind for the SPX

by Rocky White

During the last 6 months, AL-driven equity market indexes surged: KOSPI 45%, TAIEX over 30%, Nikkei225 25%, SOX 60% and S&P500 5.5% respectively.

All these markets seem attractive, but we have to bear in mind the characteristics of each market.

Among these markets, Samsung and SK Hynix comprise more than 50% of KOSPI and TSMC makes up 30% of TAIEX, which means these two markets are especially influenced by the original factors of the companies mentioned above.

Whilst there are concerns such as a decline in the price-to-sales ratio (PSR) and cash flow among hyperscalers, there has been no credit crunch; the price-to-earnings ratio (PER) does not appear overvalued, and earnings per share (EPS) also support the validity of the current share price.